Credit limits up to $50,000

(Based on creditworthiness of applicant)

Get more from your business spending with the Capital on Tap Business Credit Card, issued by WebBank. Access funds, higher credit limits, and rewards, all designed with your business in mind.

Credit limits up to $50,000

(Based on creditworthiness of applicant)

Auto-sync with accounting software

Interest rates from 16.74% APR3

(For new applicants only, based on creditworthiness)

Virtual cards available for convenient spending

$0/year

No annual fee 1

Business credit cards are specifically designed for your business expenses. They help you keep your business and personal money separate, build your company's credit history, and earn rewards on card purchases you're already making. These cards also often provide higher credit limits and features made just for business needs, like managing employee spending and integrating with accounting software.

A business credit card isn't just about spending; it's about smart financial management. Here’s how the right card, like the Capital on Tap Business Credit Card can boost your business:

Keep business and personal spending separate. This makes bookkeeping a breeze and tax time much simpler.

Every responsible use helps build a strong credit history for your company. This can open doors to better loans and financing in the future.

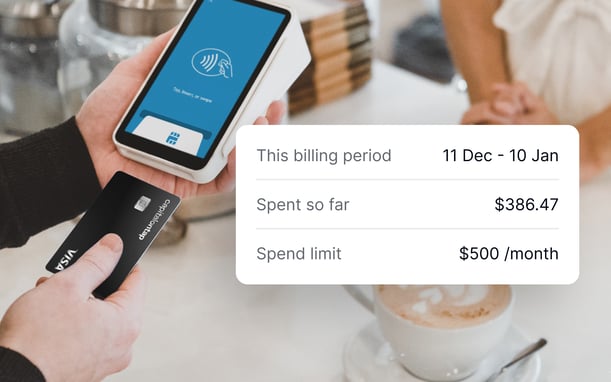

Easily track all your expenses. With features like free employee cards, you can set limits and know exactly where your business funds are going.

Earn cash back or points on everyday business purchases, from office supplies to marketing costs. It’s like getting a discount on everything you buy!1

A business credit card helps bridge cash flow gaps until payments come in. Plus, pay your balance in full by your due date each month, and there’s no interest to pay.

Business credit cards offer higher credit limits to support your growth, allowing for larger purchases and investments.

Read our customer storiesI absolutely love the leverage that the card has provided to me, and it's a much needed cushion with access to capital.

Running your business just got easier:

You'll typically get a decision within 24 hours of applying

Your physical card should arrive in just 4 business days

Virtual cards available for convenient spending

Make sure you've got all your personal and business info on hand when you apply.

To complete your application, please have these items ready:

Over 200,000 small business owners have chosen Capital on Tap for their spending needs.

Our customer stories prove why we are the best choice for your business credit card needs.

Choosing the right credit card is all about understanding your business and its unique needs. Here’s what to look for:

Be aware of common credit card fees. The Capital on Tap Business Credit Card has no annual fees, no maintenance fees, and no foreign exchange fees on US international card purchases.1

Think about your main business expenses. The Capital on Tap Business Credit Card offers 1.5% unlimited cash back on every card purchase, boosting to 2% cash back with weekly AutoPay.1

Decide if you need payment flexibility and expense tracking. The Capital on Tap Business Credit Card offers both, plus free virtual and employee cards with spend controls.

Consider your business's age and legal structure. The Capital on Tap Business Credit Card is built for established small businesses. Applying for your card won't affect your personal credit score.

Our goal at Capital on Tap is to empower small business owners by making it easier for them to run their business. A credit card can do just that by helping them optimize their cash flow, simplify their purchasing process, and give them more control over their business payments.

Business credit cards offer rewards such as cash back or points on purchases. These can be used to offset expenses or reinvest in your business.

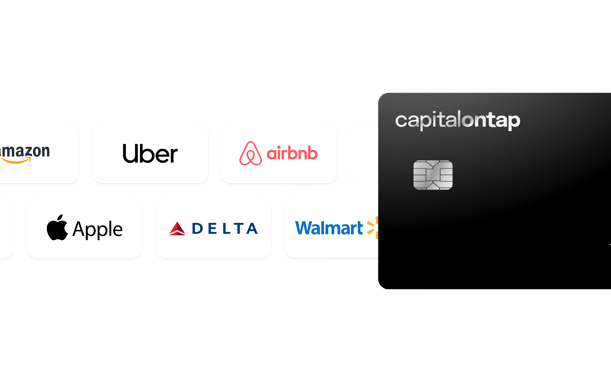

With the Capital on Tap Business Credit Card you earn 1.5% cash back on every purchase.1 You can boost it to 2% cash back by switching to weekly AutoPay.1 You can use these points to pay off your balance or even purchase gift cards from top brands like Amazon, Apple, Airbnb, and many more!1

Business credit cards should only be used to pay for business expenses. This includes things like travel costs, office supplies or paying invoices. By using a business credit card for these everyday expenses, you're not only simplifying your bookkeeping but also potentially earning benefits that can further boost your business's financial health.

Small business credit cards and corporate cards serve different needs.

Small business credit cards, like the Capital on Tap Business Credit Card, typically offer flexible terms, and the primary cardholder is responsible for the debt (though rewards are often earned by the individual). They allow carrying a balance.

Corporate cards are generally for larger companies, with the company itself responsible for all expenses, and they often require the balance to be paid in full each month. Rewards are typically earned by the business.

A company credit card allows authorized people to buy things for the business without waiting for reimbursement. Cardholders, including employees or other authorized users make purchases, but the company pays the bill. It streamlines purchasing, simplifies expense tracking, and ensures smoother cash flow for your business.

The cost of a business credit card varies widely. While some cards have annual fees that can range from zero to several hundred dollars, other potential costs include foreign exchange fees, ATM fees, and interest rates on unpaid balances. The Capital on Tap Business Credit Card stands out with no annual fees, no foreign exchange fees, and no US ATM fees. Our variable APRs range from 16.74% to 86.24%. Please see the Business Credit Card Agreement for more details.

The APR (annual percentage rate) on a business credit card can vary depending on the card issuer and your creditworthiness. Generally, business credit cards tend to have higher APRs than personal credit cards. It's important to read the terms and conditions carefully before applying for a business credit card.

Business credit cards often provide protection for card purchases that are faulty, broken, or not received. While protections can vary by issuer (as they are not personal credit cards), many, including the Capital on Tap Business Credit Card, offer safeguards against fraud, unauthorized use, and other potential issues. Always review your specific card agreement for complete details on the level of protection provided.

Yes, you can use your personal credit card for business expenses, but it's usually better to use a business credit card. Personal credit cards won't help your business build a good credit history, and they often have lower spending limits. Business credit cards come with special benefits and rewards for business owners. They can also offer features like connecting to accounting software, tracking employee spending, and virtual cards.

Yes, the majority of business credit cards can be used abroad. You can use your Capital on Tap Business Credit Card almost anywhere in the world. We don’t charge foreign exchange fees on any purchases made outside the US.1

It can take anywhere from a few minutes to a few weeks to get a business credit card; the application process varies by provider. For the Capital on Tap Business Credit Card, issued by WebBank, you can apply online in just 2 minutes. Once approved and your account is set up, your physical card should arrive in 4 business days, and virtual cards are available immediately for convenient card purchases.

The difficulty of getting a business credit card depends on your business's and personal financial profile. Established businesses with good credit history may find it easier. Newer businesses or those with less established credit might find it more challenging, often requiring a personal guaranty. With the Capital on Tap Business Credit Card, issued by WebBank, the application process is designed to be quick and straightforward for qualifying small businesses.

To qualify for a business credit card, you must be a shareholder with at least 25% ownership of your business. To apply for a Capital on Tap Business Credit Card, you will need to provide your Tax Identification Number (also known as your Employee Identification Number, or EIN), along with personal and business details, including your business's legal name, monthly revenue, and business address. If your business is an LLC, LLP, or Corporation, you are required to submit your EIN. Sole Proprietors should provide their EIN if they have one; otherwise, the owner's Social Security Number (SSN) would be accepted in lieu of the EIN.

Yes, an LLC (Limited Liability Company) is a common business structure that can qualify for a business credit card. The Capital on Tap Business Credit Card supports LLCs, along with S-Corps, C-Corps, and Partnerships, provided they meet our other eligibility criteria.

Yes, you will need a Tax ID (also known as your Employer Identification Number in most cases) to qualify for a business credit card. Businesses formalized as LLCs, LLPs, or Corporations are obligated to submit their Employer Identification Number (EIN). Sole Proprietors should provide their EIN if they have one; however, if an EIN is not available, the owner's Social Security Number (SSN) would be accepted in lieu of the EIN to qualify.

A personal guaranty is required for many business credit cards. If you default on a business credit card, it could make you personally liable for the debt and potentially negatively impact your personal credit score. Responsible use, however, can help build your business credit without negatively impacting your personal score.

The credit score needed for a business credit card considers both your personal and business credit. Personal credit scores typically range from 300 to 850, while business credit scores range from 0 to 100, with 75 or above often considered "good" by lenders. A strong personal credit score can help you qualify for a business credit card with a personal guaranty, even if your business is new.

Yes, business credit cards are an excellent way to build your business's credit history. They do this by reporting your card activity to business credit bureaus, which helps establish your company's credit risk. Using the card responsibly and paying off your balance in full each month demonstrates financial responsibility and can significantly improve your business's overall credit score, opening doors to better financing options in the future.

Building business credit is a process that takes time and consistent, responsible financial behavior. Generally, it can take anywhere from 6 to 18 months to establish a recognizable business credit profile. Key factors include making timely payments, using your business credit card responsibly, and ensuring your activity is reported to business credit bureaus.

A personal guaranty is a legally enforceable agreement that holds you personally accountable for paying off your business credit card debt. By giving a personal guaranty, you agree to take on personal liability for the debt if the company is unable to make payments. As business credit cards are a type of unsecured finance, most providers will require this type of agreement.

Yes, many business credit cards, including Capital on Tap, require a personal guaranty.

Page last reviewed on 09 October 2025