Jump to a section

When credit card balances and interest charges start accumulating, it can feel like an impossible quicksand trap—the more efforts made to get out, the deeper the debt sinks a company. Uncontrolled credit card debt can drain bandwidth, hurt cash flow, and cause sleepless nights for business owners. However, with strategy and discipline, it’s possible to recover. This blog takes you through the steps to get started.

Key takeaways

If you are struggling with business credit card debt, taking control requires decisive action and strategy. Start your recovery today by focusing on these three core areas:

-

Assessment & repayment. Objectively assess your total debt burden and implement a disciplined strategy, like the Debt Avalanche method, to pay down high-interest balances.

-

Budget & revenue. Tighten your business budget by cutting non-essential expenses and actively seek new revenue streams to allocate extra funds directly to debt repayment.

-

Negotiation & assistance. Don't go it alone. Negotiate with creditors for lower rates or seek free, impartial advice from UK debt charities like Business Debtline.

Assessing the debt situation

Before you can start work on getting out of the debt, you need to be clear on how deep of a hole you're actually in. It's time for a brutally honest assessment of where your business is at with its credit card debt.

Follow these three steps to establish your clear baseline:

-

Gather and document key data. Collect all your statements so you have them in one place, whether they’re digital or physical. Document all key info: interest rates, minimum payments, due dates, and remaining balances on each card. Organise the pile from highest rate to lowest rate.

-

Total the debt burden. Now comes the tough part: total it all up. How much does your business actually owe across all cards? This can be nerve-wracking, but you need to objectively gauge how heavy this debt burden is.

-

Gauge the impact. Crunch some quick ratios to size up the impact of this debt relative to your cash flow, revenue, and typical operating costs. Getting real about the severity of the debt gives you a crystal clear baseline.

The good news is that getting a good grasp of your situation allows you to start mapping out a comeback plan. You’ll use this debt assessment as the foundation to methodically repay balances and restore financial health.

Creating a repayment plan

With a clear picture of the debt, develop a repayment plan. How much you choose to pay depends on your business's cash flow and financial goals.

How much to pay

You can manage your credit card payments strategically to reduce interest and speed up recovery:

-

Pay the full balance. Clearing your entire balance each month (before the statement due date) is the most cost-effective approach. This allows you to avoid paying any interest charges and makes the most of interest-free periods.

-

Pay more than the minimum. Paying more than the required minimum monthly payment helps reduce your balance faster, lowers the total interest paid over time, and frees up available credit more quickly.

-

Multiple payments. You can make multiple smaller repayments throughout the month, which helps to immediately reduce your balance and potentially lower interest charges.

-

Pay the minimum amount. While this provides short-term flexibility, only paying the minimum means you will be charged interest on the remaining balance. You must at least pay the minimum amount to avoid late fees and negative impacts on your business's credit rating.

Popular repayment methods

Beyond how much you pay, there are popular methods for tackling multiple debts:

-

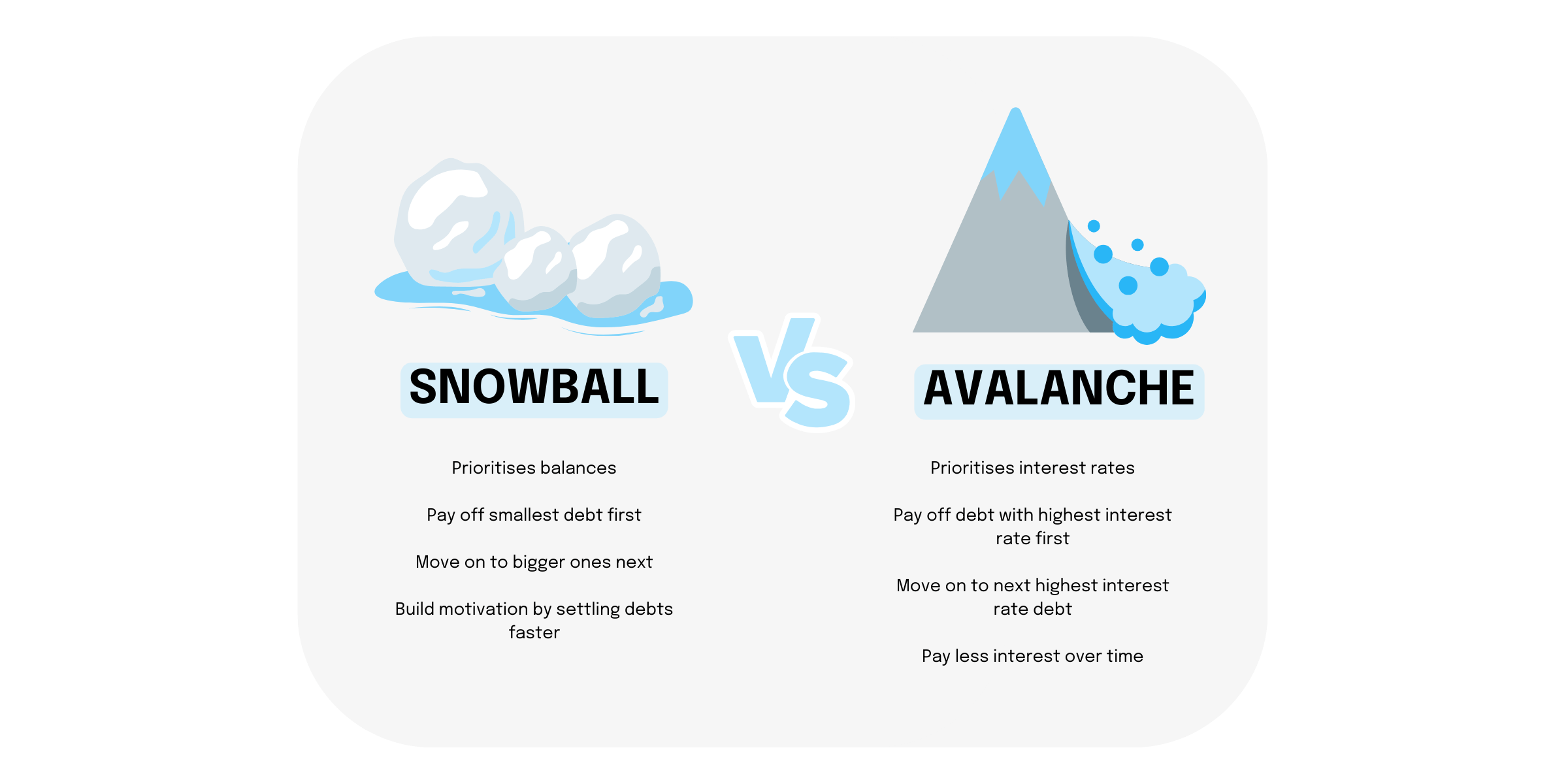

The Debt Snowball method. This prioritises paying off your smallest debt balances first, while making minimum payments on the rest. This strategy helps build motivation as you check off accounts quickly.

-

The Debt Avalanche method. This focuses on paying off the debts with the highest interest rates first, regardless of balance size. This approach reduces the total interest you pay overall and is often the most mathematically sensible way to proceed.

Choosing your strategy is just the first step. To make either method work, you need to carefully set realistic payment goals each month. Overly aggressive goals can quickly become discouraging, while undershooting can prolong the debt repayment timeline. Consider these tips when establishing your targets:

-

When setting repayment goals, be realistic about what is actually achievable each month based on your projected cash flow. Build in some buffer room rather than setting overly ambitious targets. Goals that stretch your limits are good, but make sure they are still within reach.

-

Develop a timeline with specific target dates for repaying each card based on your payment goals. Allow 3-6 months for smaller debts, and longer for larger balances. The timeline should motivate you but also recognise practical realities.

-

Map out target dates for major milestones like being 25%, 50%, or 75% of the way to paying off your total balance. Tracking these big wins will keep you motivated.

-

Continuously reevaluate the repayment plan and timeline. Adjust goals and dates if needed to keep things achievable. Staying flexible will prevent you from becoming discouraged.

Negotiating with credit card companies

Help may be possible through directly negotiating with your creditors. Credit card companies have a strong incentive to work with you to find a repayment solution that is sustainable for both sides.

Reach out to your credit card companies to explain your financial situation and discuss options to reduce the burden.

There are several potential outcomes that could provide some breathing room:

-

Lowering your interest rates. This reduces the amount going towards interest fees each month so more payments go to principal. Highlight your history of on-time payments if applicable.

-

Waiving late fees. Missed payments incur fees that then get tacked onto your balance. Ask for a one-time waiver to avoid further penalisation.

-

Reduced credit limits. Lower limits mean lower minimum payments so more can be allocated to balance reduction.

-

Balance consolidation. Transferring multiple high-rate balances to a new 0% introductory APR card saves on interest.

-

Extended repayment timeline. Negotiating a longer timeline for paying off a large balance can ease short-term burden.

The key is communicating openly about your financial realities and showing you are committed to repaying. Have account statements handy to talk specifics. Emphasise the desire to find a win-win solution so you can pay off the debt responsibility.

If you’re a Capital on Tap cardholder struggling to repay, give our friendly customer support team a call on 020 8962 7401 and they will be happy to help. We also have a dedicated specialist support team who are available to help you with your account management and offer repayment support whenever you need it.

Controlling expenses and budgeting

If you want to dig yourself out of credit card debt, you have to tighten up your budget and spending. We get it - it's not fun to cut expenses. But it's absolutely necessary if you want to free up more money to pay off those balances.

Take a good hard look at what your business is shelling out cash for every month. Are there things you can cancel or scale back? Even modest savings add up. Here are some places to start:

-

Cancel any subscriptions that aren't essential. Delete the software, video, or music services you don't really use. Downgrade plans if you can. Every pound you save contributes to the cause.

-

Renegotiate contracts with suppliers to bring costs down. You'd be surprised how much wiggle room you have.

-

Cut back on non-essential travel and entertainment. Limit meals out and trips unless they are directly generating revenue.

-

Pay attention to the little expenses too. Small Amazon charges here and there add up fast. Reign it all in.

Now, you can't just starve essential business needs and expect to thrive. The goal is redirecting savings towards debt repayment while still funding must-haves. That's where budgeting comes in…

Prioritise building a budget that allocates maximum funds to paying off cards while covering truly critical operating expenses. Treat debt repayment like any other top-level budget item.

Creating a budget takes work, but it's hugely empowering. You'll have a plan, clarity, and confidence that you're optimising spend in the best way possible while methodically reducing your debt burden.

Generating additional revenue

Trimming expenses is important, but arguably the fastest way to demolish debt is bringing in more money. Consider if there are some creative ways to boost revenue that you can dedicate to credit card balances.

If you can find untapped opportunities to increase your income streams, even a little, it can speed up your debt repayment timeline significantly.

Here are some possibilities to explore:

-

Offer something new. Diversify your product or service lineup to appeal to different customers. Find holes in your portfolio that new offerings could fill.

-

Upsell existing customers who love your core product. Provide premium add-ons and upgrades.

-

Cross-sell complementary products and services to your client base. What else would delight them?

-

Find new sales channels. Access untapped markets, whether that's online or in person. Get creative

-

Optimise your marketing promotions and ad spend to attract new business efficiently.

It’s hard work when you’re just trying to keep up with day-to-day operations, and tackling debt repayment. But carving out just a bit of time to brainstorm new revenue opportunities can work magic. Of course, be strategic - only pursue ideas that represent the highest return on your time investment.

Seeking professional assistance

Digging yourself out of a big credit card debt hole on your own is really tough. Sometimes, it pays to get professional assistance. There's no shame in reaching out for help.

Credit counselling services and debt management agencies exist to help people just like you tackle problematic balances and fees. These experts can give you guidance, moral support, informed insights and access to helpful programmes.

Here are some of the ways they can help:

-

Negotiation strategy. Provide tips and strategies for negotiating lower rates and payments with creditors. Their know-how and credibility can often get more traction than you may be able to on your own.

-

Budget optimisation. Help you optimise and streamline monthly budgets to find more opportunities for debt payments. A second set of eyes helps immensely.

-

Debt consolidation. Offer access to debt management plans that consolidate multiple payments to simplify and lower costs.

-

Resource connection. Connect you with additional resources, tools and education to help repay debt in a healthy way. You don't have to figure it all out alone.

Free, impartial UK debt advice

If you are struggling with debt, we strongly recommend you seek free, confidential, and impartial advice from an accredited organisation. These charities are authorised and regulated by the Financial Conduct Authority (FCA):

-

Business Debtline. The only free, dedicated service in the UK providing advice for self-employed people and small business owners.

-

StepChange Debt Charity. Offers comprehensive, free debt help and solutions to individuals across the UK.

-

National Debtline. Provides free, independent, and confidential debt advice via phone and webchat.

Thoroughly review whoever you decide to seek help with - check reviews, complaints, credentials, all of it.

The bottom line

Recovering from significant business credit card debt requires diligence, discipline, and using multiple strategies simultaneously. But taking decisive action can put you back on the path to financial stability. Monitor progress frequently and be prepared to make adjustments to keep momentum going. With commitment and thoughtful execution, you can overcome debt burdens and look towards future growth.

This does not constitute financial advice. If you want to understand in detail, you should speak to your financial advisor or accountant.